Maintaining the Credit Bureau Status

|

|

|

|

|

For more information about credit bureau reporting, see Credit Bureau Reporting.

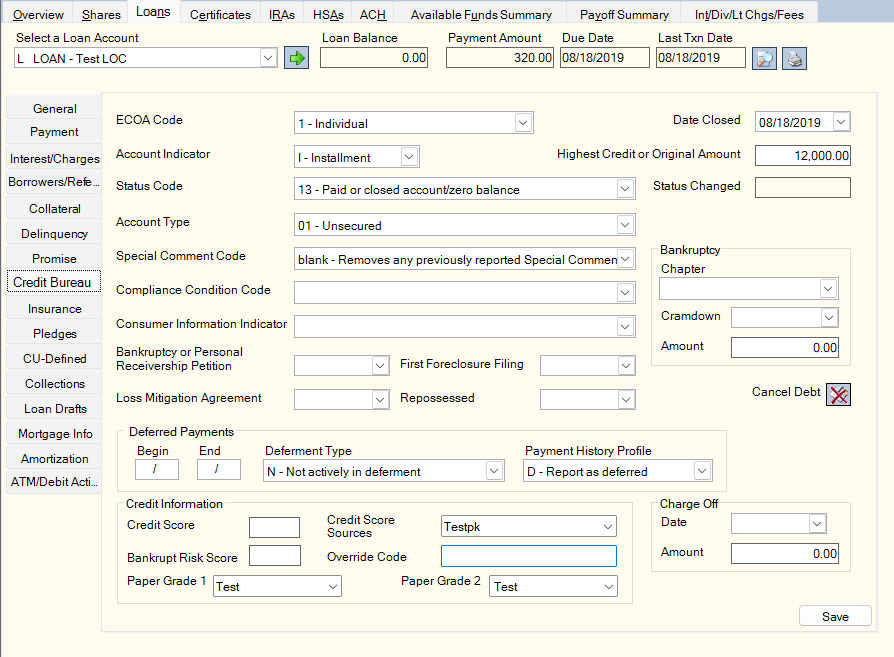

The Loans – Credit Bureau tab lets you review and maintain credit bureau information for the member loan. To access the Credit Bureau tab, under Member Services on the Portico Explorer Bar, click Account Information. The Overview tab appears on top. Click the Loans tab. Locate the member using the search tool on the top menu bar. Select the down arrow to select the search method, then enter the search criteria. Select the green arrow or press ENTER to locate the member.

Click the Select a Loan Account down arrow to select the loan note number and description. Then, click the green arrow. The General tab appears on top. Click the Credit Bureau tab.

How do I? and Field Help

Complete the following fields to maintain the credit bureau information on the Credit Bureau tab.

| Field | Description | ||

|---|---|---|---|

|

Click the down arrow to select the ECOA code that indicates how a loan is reported to the credit bureau. The valid options are: 0 - Omit from credit bureau reporting 1 - Individual (this individual has contractual responsibility for this account and is primarily responsible for its payment) 2 - Joint Contractual Liability (account for which both customer and joint borrower are contractually liable) 5 - Co-maker or Guarantor (not available when booking a new loan in Portico) 7 - Maker (co-maker liable if maker defaults) T - Terminated (not available when booking a new loan in Portico) W - Commercial / Business. Be sure to set the Address Indicator to B if W is selected. (not available when booking a new loan in Portico) X - Deceased (not available when booking a new loan in Portico) Z - Delete Customer (not available when booking a new loan in Portico) If the ECOA Code field is T, X or Z, the loan will be reported to the credit bureau one last time before no longer being reported. For Courtesy Pay loans, only values 0 and 1 are valid. The Metro 2 format is used to report consumer loans and borrowers to the credit bureaus. If the loan has an ECOA Code of W - Commercial/Business, Portico will report the first borrower with an address and an ECOA Code of 2, 5, T, X or Z in the base segment of the credit bureau transmission. If there is no borrower record with an address, the owner will be reported in the base segment of the credit bureau transmission and the loan will appear in the Exceptions section of the 350 Report. An ECOA Code of W is intended to be used when a consumer is personally liable for a business account and reported on the J2 Segment - Associated Consumer – Different Address. Keyword: RA Reporting Analytics: Loan ECOA Code (Loan folder > Loan Base query subject and Month-end Information > Loan Month-End > ME Loan Base query subject) |

|||

|

For all portfolio types, this field is used for credit bureau reporting and contains the date the account was closed to further purchases, paid in full, transferred or sold. The 350 Report Rule options determine how Portico will update this field automatically. For zero-balance loans, the ZERO BALANCE STATUS CODE / DATE CLOSED OPTIONS fields indicate how Portico will update the Date Closed field based on the type of loan specified in the Account Indicator field for status codes 11, 13, 61-65, 71, 78, 80, 82-84, 89, and 94. For loans with an Account Indicator field of L (line of credit) or C (credit card), the DATE CLOSED - LOANS WITH DRAW PERIOD AND ACCOUNT INDICATOR L OR C field on the 350 Report Rules indicates if Portico will populate the Date Closed field with the draw period expiration date for status codes 11, 13, 71, 78, 80, 82, 83, and 84. This option does not require a zero-balance on the loan. Refer to the 350 Report documentation for more details. To report a loan to the credit bureau after it has been sent as closed or if the date closed that was originally reported to the credit bureau should be modified, change the Date Closed field to blank. This will indicate to Portico that the loan should be reported to the credit bureau the next month end. For line of credit loans, a balance may be due on the loan. Keyword: CX Reporting Analytics: CB Date Closed (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|||

|

Click the down arrow to select the type of loan. Used for Shared Service Center. The valid options are: C - Credit Card I - Installment L - Line of Credit M - Mortgage Portico derives the portfolio type used in credit bureau reporting from the Account Indicator field. Any changes to the Account Indicator field may cause duplicate tradelines if the consumer reporting agencies are not notified prior to the change. Keyword: RI |

|||

|

The highest amount of credit used by the member or the original loan amount depending on the loan portfolio type. Portico will derive the portfolio type from the Account Indicator field on the Loans - Credit Bureau tab.

Reporting Analytics: Highest Credit or Original Amount (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|||

|

Click the down arrow to select the status code that indicates the current condition of the loan. Portico automatically displays codes 11, 13, 71, 78, 80, 82, and 84 based on the loan payment due date. Portico automatically displays code 97 when the loan is charged off. The 350 Report Rule options determine how Portico will update the Status Code field for zero-balance loans. For all loan portfolio types with a loan balance of 0.00, the Status Code field will be changed to 13 if the Status Code field is currently 11, 13, or 71-84. The Status Code field is updated when the credit bureau transmission is produced at month-end. For a delinquent loan, the Status Changed field reflects the date the status code was changed to indicate the loan is delinquent. For example, if a loan becomes 30 days delinquent, the status changes to 71 and this date is updated. Future changes to the status field indicating that the loan is more than 30 days delinquent will not update the date. If the status becomes current, the Status Changed field is changed to blank. Reporting Analytics: CB Status Changed Date (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) The valid options are: 11 - Current account (0-29 days past the due date) 13 - Paid or closed account/zero balance 61 - Account paid in full, was a voluntary surrender 62 - Account paid in full, was a collection account 63 - Account paid in full, was a repossession 64 - Account paid in full, was a charge-off 65 - Account paid in full. A foreclosure was started. 71 - Account 30-59 days past the due date 78 - Account 60-89 days past the due date 80 - Account 90-119 days past the due date 82 - Account 120-149 days past the due date 83 - Account 150-179 days past the due date 84 - Account 180 days or more past the due date 88 - Claim filed with government for insured portion of balance on a defaulted loan 89 - Deed received in lieu of foreclosure on a defaulted mortgage; there may be a balance due 93 - Account assigned to internal or external collections 94 - Foreclosure completed; there may be a balance due 95 - Voluntary surrender; there may be a balance due 96 - Merchandise was repossessed; there may be a balance due 97 - Unpaid balance reported as a loss (charge-off) DA - Delete entire account (for reasons other than fraud) DF - Delete entire account due to confirmed fraud (fraud investigation completed) 05 - Account transferred (obsolete) If a loan is currently in a deferment or accommodation period., the Status Code field on the Loans - Credit Bureau tab will reflect the actual calculated or manually-entered status code, which may not match the status code that is reported in the credit bureau transmission. On the 350 Report, exception codes 04 and 06 will appear to indicate that maintenance is required to discontinue reporting the loan to the credit bureau.

Keyword: RS Reporting Analytics: CB Status Code (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|||

|

Click the down arrow to select the account type reported to the credit bureau. The codes are provided by Associated Credit Bureaus, Inc. Types marked obsolete are no longer supported. The valid options are:

Keyword: RT Reporting Analytics: CB Account Type (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|||

|

Special Comment Code |

Select the Associated Credit Bureaus, Inc. Special Comment Code. This description is used in conjunction with the Status field to further define the account for credit bureau reporting. The valid options are: Blank - Removes any previously reported special comment code B - Account payments managed by Credit Counseling Service C - Paid by co-maker H - Loan assumed by another party I - Election of remedy M - Account closed at credit grantor's request O - Account transferred to another lender S - Special Handling. Contact credit grantor for additional info V - Adjustment pending AB - Debt being paid through insurance AC - Paying under a partial or modified payment agreement AH - Purchased by another lender AI - Recalled to military active duty AM - Account Payments Assured by Wage Garnishment AN - Account acquired by RTC/FDIC AO - Voluntarily surrendered, then redeemed AP - Credit line suspended AS - Account closed due to refinance AT - Account closed due to transfer AU - Account paid in full for less than the full balance AV - First payment never received AW - Affected by natural disaster AX - Account paid from collateral AZ - Redeemed repossession BA - Transferred to recovery. Requires Status code 71-97 BB - Full termination/status pending. Requires account type 3A (Auto Lease) or 13 (Lease) BC - Full termination/obligation satisfied. Requires account type 3A (Auto Lease) or 13 (Lease) BD - Full termination/balance owing. Requires account type 3A (Auto Lease) or 13 (Lease) BE - Early termination/status pending. Requires account type 3A (Auto Lease) or 13 (Lease) BF - Early termination/obligation satisfied. Requires account type 3A (Auto Lease) or 13 (Lease) BG - Early termination/balance owing. Requires account type 3A (Auto Lease) or 13 (Lease) BH - Early termination/insurance loss. Requires account type 3A (Auto Lease) or 13 (Lease) BI - Involuntary repossession. Requires account type 3A (Auto Lease) or 13 (Lease) BJ - Involuntary repossession/obligation satisfied. Requires account type 3A (Auto Lease) or 13 (Lease) BK - Involuntary repossession/balance owning. Requires account type 3A (Auto Lease) or 13 (Lease) BL - Credit card lost or stolen BN - Paid by company who originally sold the merchandise BO - Foreclosure proceedings started BP - Paid through insurance. Requires Status code 13 or 61-65 and a current balance of 0.00. BS - Prepaid Lease - Consumer Paid In Advance BT - Principal deferred/interest payment only CH - Guaranteed/Insured CI - Account closed due to inactivity CJ -– Credit line no longer available in repayment phase. Not valid for account statuses 13 and 61-65. CK - Credit line reduced due to collateral depreciation CL - Credit line suspended due to collateral depreciation CM - Collateral released by creditor/balance owing. Not valid for account statuses 13 and 61-65. CN - Loan modified under a federal government plan CO - Loan Modified CP - Account in Forbearance CS - Used by Child Support Agencies Only when reporting collection accounts (No actual comment displays) DE - Debt extinguished under state law. Not valid for account statuses 13 and 61-65. After Portico reports the loan in the credit bureau transmission, stop reporting the loan by changing the ECOA code to 0. ZZ - Internal - Stops charged off loans from being paid off on the 632 Report Keyword: RR Reporting Analytics: CB Special Comment Code (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

||

|

Click the down arrow to select the condition code required for legal compliance according to the Fair Credit Reporting Act (FCRA) or Fair Credit Billing Act (FCBA). The valid values are: Blank - Not Applicable - System Default XA - Account closed at consumer's request XB - Account information disputed by consumer XC - Complete investigation of FCRA dispute - consumer disagrees XD - Account closed at consumer's request and in dispute under FCRA XE - Account closed at consumer's request and dispute investigation complete, consumer disagrees XF - Account in dispute under Fair Credit Billing Act XG - FCBA dispute resolved - consumer disagrees XH - Account previously in dispute - now resolved, reported by credit grantor XJ - Account closed at consumer's request and in dispute under FCBA XR - Removes the most recently reported Compliance Condition Code Keyword: CC |

|||

|

Click the down arrow to select the bankruptcy status reported to the credit bureau for the borrower. The valid options are: Blank - Not Applicable - System default A - Petition for Chapter 7 Bankruptcy B - Petition for Chapter 11 Bankruptcy C - Petition for Chapter 12 Bankruptcy D - Petition for Chapter 13 Bankruptcy E - Discharged through Bankruptcy Chapter 7 F - Discharged through Bankruptcy Chapter 11 G - Discharged through Bankruptcy Chapter 12 H - Discharged through Bankruptcy Chapter 13 Q - Removes Bankruptcy Indicator previously reported (A through P) R - Reaffirmation of Debt S - Removes Reaffirmation of Debt and Reaffirmation of Debt Rescinded Indicators (R,V,2A) previously reported T - Credit Grantor Cannot Locate Consumer U - Consumer Now Located (removes previously reported T indicator) V - Chapter 7 Reaffirmation of Debt Rescinded 2A - Lease Assumption I - Chapter 7 Bankruptcy Dismissed (obsolete) J - Chapter 11 Bankruptcy Dismissed (obsolete) K - Chapter 12 Bankruptcy Dismissed (obsolete) L - Chapter 13 Bankruptcy Dismissed (obsolete) M - Chapter 7 Bankruptcy Withdrawn (obsolete) N - Chapter 11 Bankruptcy Withdrawn (obsolete) O - Chapter 12 Bankruptcy Withdrawn (obsolete) P - Chapter 13 Bankruptcy Withdrawn (obsolete) Consumer Information Indicator values Q, S, and U are not intended to be reported to the credit bureau on a recurring basis. After they are sent to the credit bureau, Portico will change the Consumer Information Indicator field to blank. Keyword: CI |

|||

|

A date must be entered in the Bankruptcy or Personal Receivership Petition field if the Consumer Information Indicator field is A - H (Bankruptcies) or V-Y (Reaffirmation of Debt Rescinded with Bankruptcy Chapters). Click the down arrow to select the date from the pop-up calendar or enter the date in MM/DD/YYYY format. The date must be the current date or earlier; it cannot be a date in the future. If a valid date is not entered for loans where the Consumer Information Indicator field is A - H (Bankruptcies) or V-Y (Reaffirmation of Debt Rescinded with Bankruptcy Chapters), an error message will appear when maintenance is attempted on the loan. The date of first delinquency on the loan derived from the Status Changed field or the Bankruptcy or Personal Receivership Petition field on the Loans - Credit Bureau tab will be reported in the credit bureau transmission and 350 Reoprt, depending on the status code, payment rating and consumer information indicator.

If none of these conditions are met, zero will be reported in the credit bureau transmission. If zero reported in the credit bureau transmission, the 1ST DLQ field will be blank on the 350 Report. Therefore, a date may appear in the Status Changed field or the Bankruptcy or Personal Receivership Petition field on the Loans - Credit Bureau tab, but it will not appear in the 1ST DLQ field on the 350 Report. Keyword: BR |

|||

|

The date when the member agreed to any loss mitigation program. Click the down arrow to select the date from the pop-up calendar or enter the date in MM/DD/YYYY format. If date appears in this field, a special disclosure will be printed on the mortgage loan statement (472 Report). Keyword: MI |

|||

|

The date when the servicer made first notice or filing of any judicial or non-judicial foreclosure process. Click the down arrow to select the date from the pop-up calendar or enter the date in MM/DD/YYYY format. If date appears in this field, a special disclosure will be printed on the mortgage loan statement (472 Report). Keyword: FE |

|||

|

The date of repossession for loans with an account status of either 96 - Merchandise was repossessed; there may be a balance due or 63 - Account paid in full, was a repossession. |

The Deferred Payments group box lets you set up a deferment or accommodation period for a loan.

| Field | Description |

|---|---|

|

The month and year that the deferment should begin. The deferment or accommodation period will begin on the first day of the month. For skip payment processing, Portico will use the date in the Skip Begins field, the payment due date prior to the skip period, the payment frequency, and the number of payment periods to advance to complete the Deferred Payments Begin and End Date fields in the back-office cycle. When a loan with a payment frequency of weekly, bi-weekly, or semi-monthly has skip payments, a deferment or accommodation period will only be built when payments for an entire month are skipped. The deferral period for skip payments will be built for the month(s) the skips are scheduled to be processed. The Deferred Payments Begin field is the first month where all payments are skipped, and the Deferred Payments End field is the last month where all payments are skipped. For delinquent loans, Portico will build the deferment period record in the month-end cycle of the month that the first payment should be skipped. For paid-ahead loans, the deferment period record will be built when a payment is applied, but the deferment period encompasses future payment due dates that will be skipped. When online payments, advances, and immediate skips trigger the skip payment process, Portico will update the Deferred Payments Begin and End fields in the next back-office cycle. If a loan is currently in a deferment or accommodation period and the loan is also set up with a skip payment during the deferment or accommodation period, the deferment or accommodation period takes precedence. Portico will not update the Deferred Payments Begin and End fields when a payment is made on the loan that triggers the skip payment process to advance the payment due date. If a loan's deferment/accommodation period is set for the future and the loan is also set up with a skip payment, the deferment or accommodation period takes precedence. Portico will not update the Deferred Payments Begin and End fields when a payment is made on the loan that triggers the skip payment process to advance the payment due date. If a loan's deferment/accommodation period has expired and the loan is also set up with a skip payment that takes affect after the deferment/accommodation period, the skip payment takes precedence. Portico will update the Deferred Payments Begin and End fields when a payment is made on the loan that triggers the skip payment process to advance the payment due date. If a loan is setup with multiple skip payments (e.g. two skip payments) and a single transaction covers two loan payments, the skip payment process will advance the due date two times. Although a single transaction caused the activation of both skip payments, Portico will only use the skip information of the first skip payment to automatically complete the Deferred Payments Begin and End fields. Reporting Analytics: Deferred Payment Begin Date (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|

|

The month and year that the deferment should end. The deferment or accommodation period will end on the last day of the month. For skip payment processing, Portico will use the date in the Skip Begins field, the payment due date prior to the skip period, the payment frequency, and the number of payment periods to advance to complete the Deferred Payments Begin and End Date fields in the back-office cycle. When a loan with a payment frequency of weekly, bi-weekly, or semi-monthly has skip payments, a deferment or accommodation period will only be built when payments for an entire month are skipped. The deferral period for skip payments will be built for the month(s) the skips are scheduled to be processed. The Deferred Payments Begin field is the first month where all payments are skipped, and the Deferred Payments End field is the last month where all payments are skipped. For delinquent loans, Portico will build the deferment period record in the month-end cycle of the month that the first payment should be skipped. For paid-ahead loans, the deferment period record will be built when a payment is applied, but the deferment period encompasses future payment due dates that will be skipped. When online payments, advances, and immediate skips trigger the skip payment process, Portico will update the Deferred Payments Begin and End fields in the next back-office cycle. If a loan is currently in a deferment or accommodation period and the loan is also set up with a skip payment during the deferment or accommodation period, the deferment or accommodation period takes precedence. Portico will not update the Deferred Payments Begin and End fields when a payment is made on the loan that triggers the skip payment process to advance the payment due date. If a loan's deferment/accommodation period is set for the future and the loan is also set up with a skip payment, the deferment or accommodation period takes precedence. Portico will not update the Deferred Payments Begin and End fields when a payment is made on the loan that triggers the skip payment process to advance the payment due date. If a loan's deferment/accommodation period has expired and the loan is also set up with a skip payment that takes affect after the deferment/accommodation period, the skip payment takes precedence. Portico will update the Deferred Payments Begin and End fields when a payment is made on the loan that triggers the skip payment process to advance the payment due date. If a loan is setup with multiple skip payments (e.g. two skip payments) and a single transaction covers two loan payments, the skip payment process will advance the due date two times. Although a single transaction caused the activation of both skip payments, Portico will only use the skip information of the first skip payment to automatically complete the Deferred Payments Begin and End fields. Reporting Analytics: Deferred Payment End Date (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|

|

Indicates if a loan is currently in a deferment or accommodation period. The valid values are: M - Standard deferment (The deferment or accommodation period is manually set up by the credit union. Portico will report the account status code as 11 and the amount past due as 0.00 in the credit bureau transmission. Portico will store the account status code and amount past due that would have reported if the loan was not in a deferment or accommodation period.) N - Not actively in deferment (System default. Portico will store the account status code and amount past due reported in the prior month.) P - Prior values reported in deferment (Portico will store the account status code and amount past due reported for the loan the month prior to the deferment period. The stored values will be reported in the credit bureau transmission unless the loan becomes current or paid off during the deferment period. In the month the loan comes out of deferment, Portico will store the account status code and amount past due that would have reported if the loan was not in a deferment or accommodation period.) S - Skip payment deferment (The deferment or accommodation period is set up by skip payment processing in the back-office cycle. Portico will report the account status code as 11 and the amount past due as 0.00 in the credit bureau transmission. Portico will store the account status code and amount past due that would have reported if the loan was not in a deferment or accommodation period.) Reporting Analytics: Deferment Type (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

|

|

Loan payments that are reported in the credit bureau transmission as deferred should be reported with a D in the Payment History field in the credit bureau transmission. The Payment History Profile field lets you override the default value of D and report the loan with a value of 0 indicating the account is current. The valid values for the Payment History Profile field are: D - report payment as deferred 0 - report payment as current If the Payment History Profile field is 0 and the amount past due for the loan calculated that month end is greater than 0.00, the loan will be reported in the credit bureau transmission as deferred (D) not current. Reporting Analytics: Payment History Profile (Loan folder > Credit Bureau query subject and Month-end Information > Loan Month-End > ME Credit Bureau query subject) |

For a bankrupt loan, you can select the type of bankruptcy and enter the amount and date that the bankruptcy court ordered a bankrupt loan to be cramdowned.

| Field | Description |

|---|---|

|

Click the down arrow to indicate that the loan is in bankruptcy and select the type of bankruptcy. The valid options are:

If 7, 11 or Unknown is selected, the Loan Mortgage Statement Report 472 will generate a specially-formatted mortgage statement. If 12 or 13 is selected, a specially-formatted mortgage statement will not be created. Instead, exception code BK will appear on the Loan Payment Recalculation Report 460 and Adjustable Rate Mortgage Report 470 if the member did not opt out of receiving a statement (the Opt Out Requested field on the Loans - General tab is blank). The exception code indicates that the credit union must create a statement manually, if needed. Keyword: BF |

|

|

The date the court ordered the cramdown on a bankrupt loan. Click the down arrow to select the date from the pop-up calendar or enter the date in MM/DD/YYYY format. |

|

|

The amount that the bankruptcy court ordered a bankrupt loan to be "cramdowned" to. This is the value the bankruptcy court has decreed upon the collateral. Length: 7 numeric |

To update the credit information for the loan, complete the following fields:

| Field | Description |

|---|---|

|

The credit score for the loan as defined by the credit union. Keyword: SC Length: 5 numeric Security Permission: Loans - Field - Credit Score - View Restricted Security Group: Loan Level Credit Score - User is View Restricted |

|

|

The bankruptcy risk score for this account. The member bankruptcy risk score is defined by the credit union Keyword: BK Length: 4 alphanumeric |

|

|

The source of the credit score. Keyword: CS Length: 10 alphanumeric |

|

|

The individual override code for this account. The member individual override code field is defined by the credit union and is informational only. Keyword: IO Length: 4 alphanumeric |

|

|

The grade for a loan from the current credit bureau reporting agency. Most credit services use codes A through E; however, credit unions can have their own definitions and uses for paper grade codes. Characters A through Z and numbers 0 through 9 may be used. Special characters are not allowed. Keyword: PG Length: 1 alphanumeric |

|

|

The grade for a loan from the previous credit bureau reporting agency. Most credit services use codes A through E; however, credit unions can have their own definitions and uses for paper grade codes. Characters A through Z and numbers 0 through 9 may be used. Special characters are not allowed. Keyword: P2 Length: 2 alphanumeric |

For a charged-off loan, you can enter the amount and date that the loan was charged off.

Click Save to save your changes.

Click the Cancel Debt icon button to display the Cancellation of Debt dialog box and report cancellation of debts to your members and the IRS using form 1099-C.

To access and maintain the member's ownership information, users must be assigned to one of the following pre-defined security groups or you can create your own security groups. You can add these permissions to a credit union-defined security group using the Security Group Permissions – Update window.

| Permissions | Security Groups |

|---|---|

| Loans - Tab - Credit Bureau - Maintain |

Lending - Manager |

| Loans - Tab - Credit Bureau - View Only |

Lending - Clerk |

| Loans - Field - Credit Score - View Restricted | Loan Level Credit Score - User is View Restricted |

To ensure that the base credit bureau information is available for future reporting, a credit bureau record is built for new loans regardless of the ECOA Code value defined on the New Loan - Setup tab. The credit bureau record is built using the following default values:

| Field | Default |

|---|---|

| Special Comment Code | Blank |

| Account Type | Blank |

|

Account Indicator |

use the default value for the loan type from the Loan Profile |

|

Status Code |

11 |

|

Delinquency History |

Blank |

Portico Host: 642, 64M, 68M, LINQ (683)